Jordanian Banks in 2021

Winners of the pandemic

Jordanian banks are relatively small in comparison to their counterparts in the region or the world. On the other hand, there are over 25 banks in the country, both commercial and Islamic, which is a large number compared to other countries, especially developed ones. To German economist Richard Werner, Jordan is manifesting the free market dream of having small local and cooperative banks that are not too big too fail and a systemic risk to a nation.

Let’s see how the banks faired in 2020-2021, if they are still a safe investment and why they have been the biggest winners since the Second Gulf War

Outstanding Performance

Despite the contraction in GDP caused by the pandemic in 2020, most banks proved not only to be resilient but they outperformed and exceeded expectations, thanks in part to CBJ’s early intervention.

Main Indicators of the banking sector:

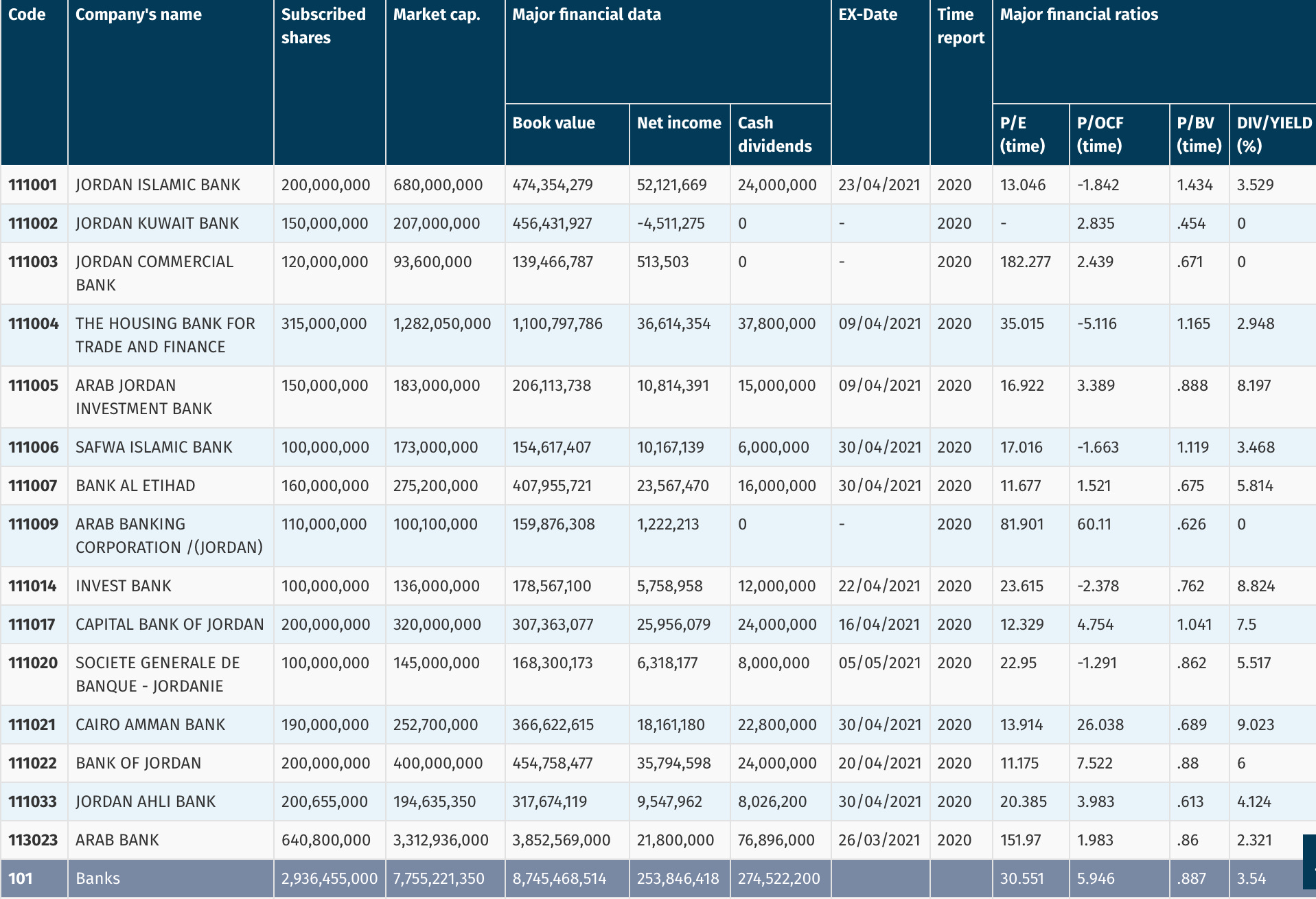

-Stock market results of the 15 listed banks shows that net profits grew by 77% in the first half of 2021 compared to the same period of 2020.

-Dividends paid out totalled 274 million JODs (3.54% yield)

Source: ASE Monthly Bulletin

-Bank assets (to banks, assets are loans to other parties and their liabilities are deposits) grew 5.1% to reach 56.4 billion.

-Jordan enjoys one of the highest Deposit/GDP ratios in the world.

-Non-performing Loans grew slightly during the pandemic: 5.5%

-Liquidity ratio stood at 136.5% (well above the minimum 100% required according to Basel III)

Source: CBJ Financial Soundness Indicator

Rating Agencies such as Fitch, Moody’s and Standard&Poor’s all rate the banks on-par and even higher than the Jordanian Government’s rating.

All seems stellar for the banking sector.

Future Outlook

The banking sector was one of the best return in investment during the past two decades. It is said that the Jordanian banks’ true Equity is Trust, earned and granted by the depositors; and that the banking sector is the main foundation and skeletal structure of the economy. In the Amman Stock Exchange, the banking sector represents 49% of the total market capitalisation of the stock market. It is the sector that developed the fastest, keeping up with international trends and standards, and has grown substantially and managed to weather most crises in the region.

But the sector faces three important and fundamental issues:

Debt imprisonment which is a big topic to be covered in a separate letter. But the main gist of it is that banks are currently lending risk free when the lender can imprison his debtor. In Jordan, Credit Risk management is not utilised to its full capacity.

High interest rates: When the annualised GDP growth is below the the prime lending rate, this means that the economy in general and businesses in particular are not growing fast enough to pay off their debts (that are growing faster).

Real Estate on the Balance Sheets: With high interest rates, low growth, and debt imprisonment comes asset seizures. During an economic downturn, many businesses fail and their assets are seized, mostly real estate. When banks seize these assets, they are forced to sell them all at once, causing a fire sale. Jordan’s real estate prices could crash, becoming a burden both to the lender and the debtor (whose asset is now worth less than the debt and falls into a debt trap). Some speculate that the recent announcement of the Bank Fund is actually to set up a “bad bank” to act as a sponge to all distressed real estate assets.

These three aspects need to be addressed soon for the sake of both the well being of the economy in general and the banks in particular.

As bank al Etihad and Jordan Kuwait bank are evaluating a merger, quite interested to hear your thoughts on this idea and its implications to the competitive landscape for example