Shadow (micro) Banking

A ticking time bomb

Korean culture is captivating the world with its music, books and tv shows. The K-pop group BTS recently performed at the United Nations assembly1; the Korean film “Parasite” won the Oscar for best foreign film in 2020; and a new hit show called “Squid Game” is breaking world records for Netflix2.

What the last two have in common is the world of predatory lending and loan sharks3: how some people need to get loans from informal lenders to get by, only to find out they are burdened by never ending debt and would do the impossible to escape their debt trap. The message seems to resonate with a lot of people around the world.

In Jordan, microfinancing is gaining traction and growing at an incredible pace. But are the local lending firms applying the same predatory tactics as the ones seen on screen? Let’s find out.

Legal Usury or Riba4

I will not dwell into the theological and philosophical discussions on usury5, but will assume here that any interest rate on a loan that is double that of the prime lending rate (PLR) of commercial banks is considered usury (including all extra charges associated with the loan).

The current PLR is 7.75%6 (while the CBJ Main rate is 2.5%)

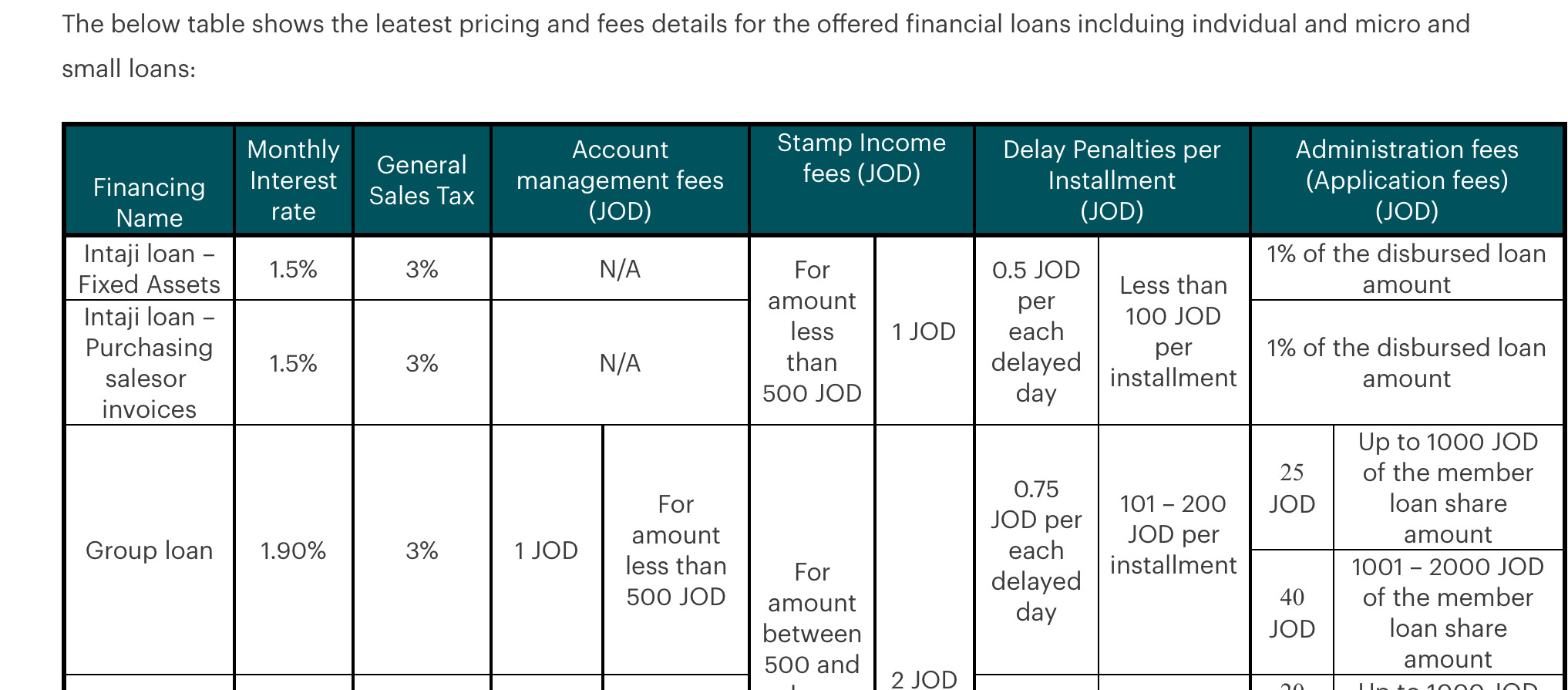

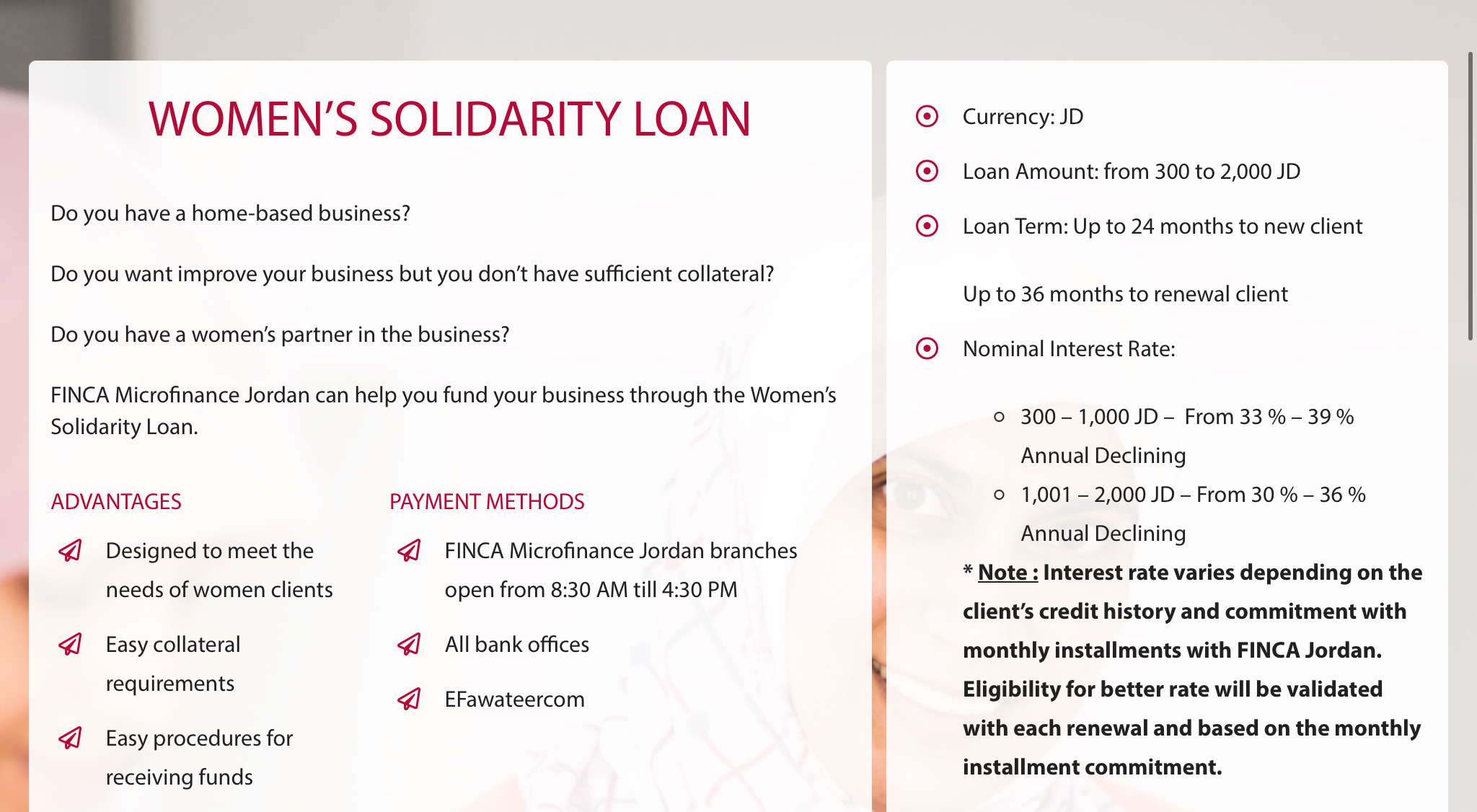

Looking at the two largest microfinancing firms, Ahli Micro7 and Finka :

So for example, a person takes out a 500 JOD loan for 24 months, that person would need to pay 45% interest on the loan. This does not include any additional fees that are subtracted before the loan is even paid out to the customer.

Of course at first glance, the interest is much lower than “payday” loans in the USA that range between 300-600% APR. But as anyone knows, the debt accumulates when you add in penalty fees, followed by court fees, legal fees etc.

According to some legal experts, microfinancing companies are using predatory tactics if the debtors miss a loan payment. Just like loan sharks, they would harass the client at their homes or their places of work, continuous threatening phone calls etc. One lawyer has shown that on a daily basis, more than 50 new people are being pursued by the legal system for failing to pay their micro loans. And the majority of the debtors are women:

Let sleeping dogs lie

In 2006, Muhammad Yunus8 won the Nobel Peace Prize for creating the system of “micro lending”. This is the same year when micro loan firms started growing at an incredible pace in Jordan.

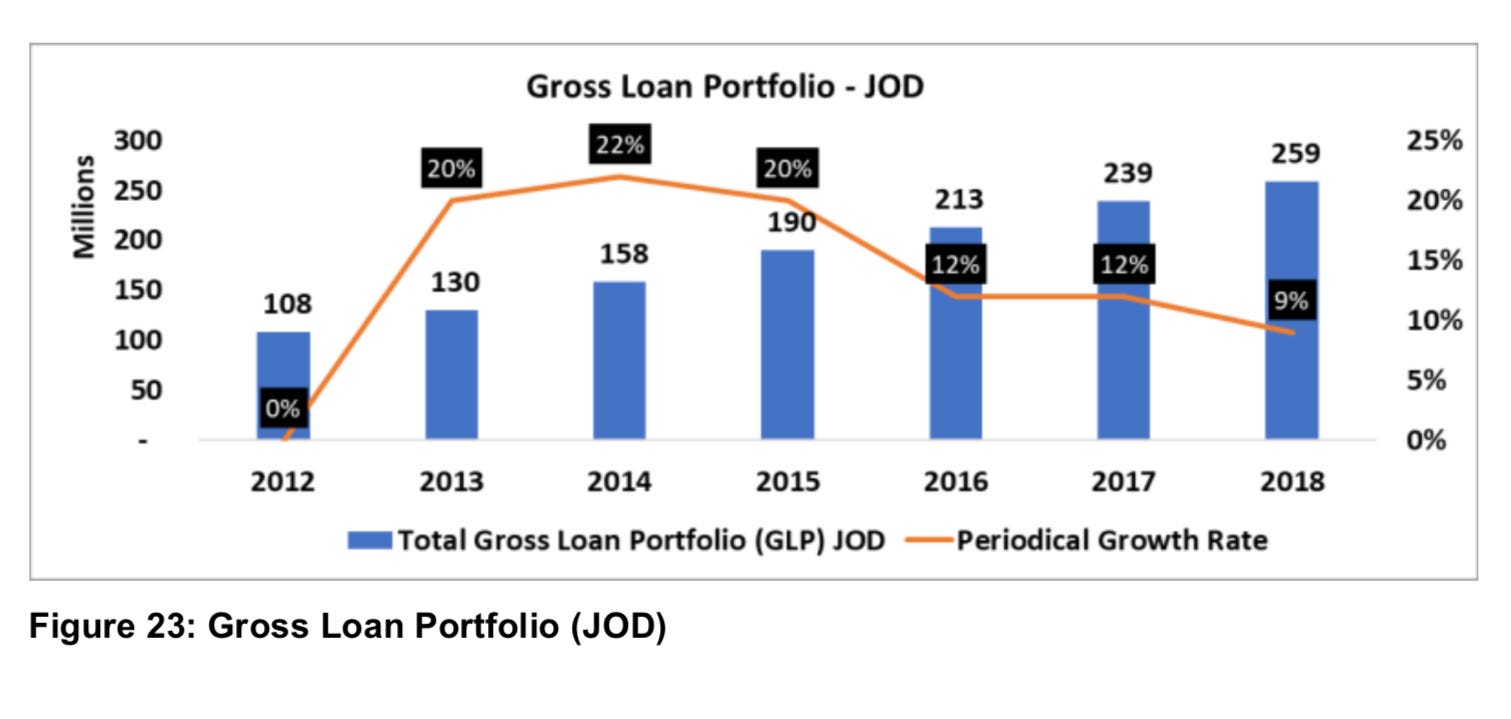

By 2018, the gross loan portfolio of microfinanciers was 260 million JODs. That is below 1% of bank credit. Yet the reader has to bear in mind that the average loan size is around 500 JODs, and most loans are “group loans” that come with several guarantors to the micro loan. This means that we are talking of more than half a million borrowers. And most of these monies were simply used to pay off for daily needs (food, electricity bills, old debts).

Not a (Squid) Game

The initial intention of microfinancing firms might have been noble: helping those with lower income or refugees get access to credit, raise financial inclusion outside the cities, help women from remote areas start a business etc.

But it turns out that microfinancing firms are actually doing the opposite: Preying on the financial illiterate for massive profit.

Unless these companies do not change their attitude, they will soon find a growing number of unhappy borrowers sitting in jail plotting their revenge. This is a serious societal problem that needs to be addressed immediately.

In the meantime, this is the opportune moment for commercial and Islamic banks to step in using technology:

-financial exclusion now can be addressed since mostly everyone has a basic smartphone to use

-financial illiteracy can also be addressed by free online courses by these banks using social media

-give out small loans at competitive rates: PLR 7.75% + a small risk percentage

It might be not as profitable for banks to issue such a large number of small risky loans especially with all the paperwork, but it could prove beneficial down the line.

Access to credit is unofficially considered as a human right, and no company should take advantage of it.

For a more detailed study of Micro Financing in Jordan, I suggest reading the following (starting from page 51): Tanmeyah

https://news.un.org/en/story/2021/10/1102252

https://observer.com/2021/10/netflix-squid-game-viewership-ratings-bridgerton-witcher-stranger-things/

https://www.nylon.com/life/squid-game-debt-crisis-south-korea

https://www.investopedia.com/terms/r/riba.asp

https://socialsciences.mcmaster.ca/econ/ugcm/3ll3/bentham/usury

https://www.jkb.com/content/interests-fees

https://amc.com.jo/en/pricing-and-fees-list

https://www.nobelprize.org/prizes/peace/2006/yunus/biographical/