Bank Etihad and Jordan Kuwait Bank

Merger of equals?

Before any merger was officially announced1, there were rumours circulating days prior on WhatsApp. Yet al Rai economist published his column hours before the official announcement in the stock market (maybe some WhatsApp rumours are to be believed…)

He tackled it straight on with the numbers: if both are combined, they will become the 2nd biggest bank in Jordan after Arab Bank (putting Housing Bank in 3rd place).

Numbers

If we were to combine both banks, from a revenue perspective, they would make 885 mil JODs which is more than Housing Bank’s (THBK) measly 622 mil JODs. Albeit THBK’s revenue grew 30% YoY. [Jordanian Banks overall had a spectacular year thanks to higher rates2. Contrary to US banks3. 🪬]

Their combined assets and deposits will be 50% larger than Housing Bank’s.

But the market cap of the new horizontal entity will still be half of Housing Bank! 🤔

Open Book

At first glance, the prospective merger feels like an arranged marriage within the banking cartel between two incompatible individuals.

One is young, hip, swift, progressive, self-made, that can implement a strategy flawlessly (by young and progressive: I mean that the majority of employees still have their hair and one that has the highest female workforce in the banking industry standing at 45%4)

The other is Gulf-backed ☕️ catching up to modern times.

For this union to work however, one has to remember that all successful relationships are based on honesty5: both banks, when it comes to digging deeper and evaluating their books, need to show each other’s skeletons in the closet.

I would love to be a fly in the wall when these discussions take place: (this is just a fictional account not based on real events)

Bank A: “So you know that building we sequestered from that bankrupt hospital? We’ve been trying to sell it with no luck. We still didn’t take any provisions on it. Hope that’s okay.”

Bank B: “Interesting… You know that big customer deposit we have. We are not technically paying any interest on it 😉. Hope that’s okay too”.

The union of these 2 seemingly different banks (no common shareholders, no common foreign markets) will hopefully create a new clean, strong, and transparent entity that can grow both domestically and regionally. A new bank with new solid foundations can weather any storm. I for one am excited about this, maybe the CBJ will be too and give its blessing.

Other Considerations

Banks are also competing in the digital sphere.

Bank Etihad is way ahead in the game, which could be beneficial to Jordan Kuwait Bank.

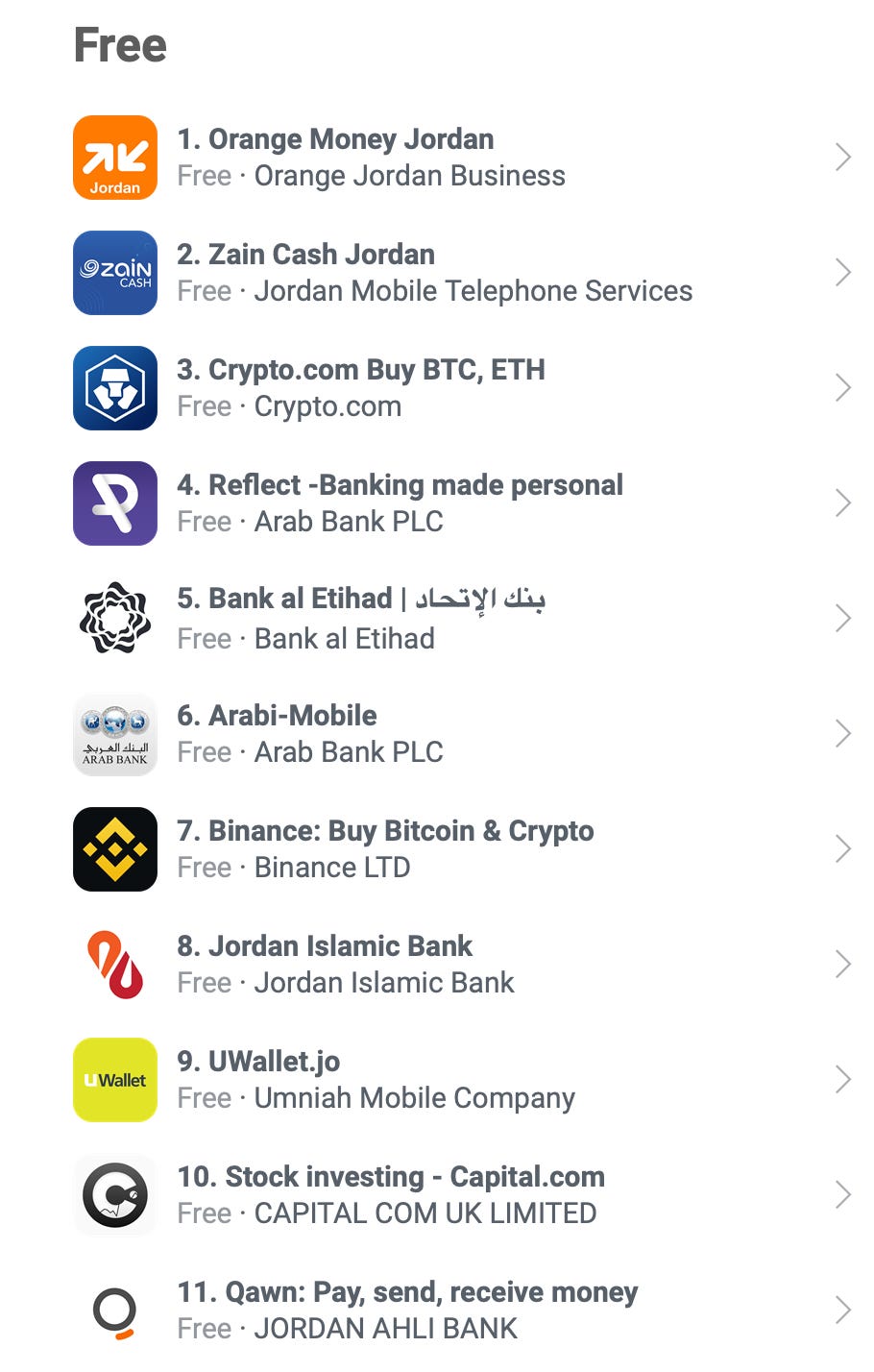

Looking at the top 10 finance apps on Android in Jordan, Arab Bank’s Reflect app is the most downloaded. Etihad’s app is not that far behind at number 7 while Kuwait Bank is nowhere to be seen.

For iPhone, Etihad and Reflect are tête-à-tête.

Etihad bank is also dominating in the Point-of-Sale market, rivalling Arab Bank (like David v. Goliath)

Jordan Kuwait on the other hand can offer its potential partner its long list of legacy clients.

I personally hope both will create a new super app that will also allow average customers to easily invest in the Amman Stock Market (and not one to invest in TSLA 0.00%↑ or NVDA 0.00%↑ 6 ).

Eventus stultorum Magister

In Jordan, when one opens a shawarma shop and it becomes hugely popular, it won’t be long before 10 imitating competitors pop up right next to it.

Same goes for banking. When Capital Bank successfully issued perpetual bonds, it wasn’t long before Jordan Kuwait Bank and Etihad followed. Capital set the precedent and it was a case study for the sector (same goes for foreign bank acquisitions).

Now if this merger proves to be successful, this could open doors for more mergers and consolidation in the industry, (maybe next year we will celebrate the union between Ahli and Commercial bank?)

February 22 2024: https://x.com/jordanfinance/status/1760616806279004513?s=20

Female workforce in the Jordan Kuwait Bank is 38% (close to industry average). The lowest is Jordan Islamic Bank at 15%.

The ‘story’ of the Chinese man who divorced his wife because she lied about her ugly past and the plastic surgery she did, is always a good moral lesson: https://www.snopes.com/fact-check/man-sues-wife-ugly-children/

https://www.bankaletihad.com/en/knowledge-hub/trading-stocks/

I believe this deal will be a bit complex, the two cultures are very far off of each other. BAE very progressive, chilled (somewhat compared to other banks), while JKB is more of rigid. The fact that they’ll end up with more than 100 branches that will require mass level closures and a big number of redundant frontliners will need some guts to handle them in light of the CBJ mandates to not let go people for 24 months.

Add to that the fact that since they are two medium sized banks middle and upper management will be pressured to prove their existence and the need to be kept under the new umbrella … the case in Capital vs Audi and SGBJ was easier since branches and ATMs were much less, employees were more under control as count.

But BAE will definitely benefit from the regional presence that JkB enjoys will availing technology solutions to them across the different geographies without having to pay additional capital raises