Impact of MSCI listing

Déjà vu

We Jordanians tend to have a short memory: we tend to forget the recent achievements or scandals of the government/politicians and business sector. We seem to move from one achievement/scandal to the next, forgetting the one before it and rarely seeing the bigger picture.

For example, when Morgan Stanley Capital International listed Jordan Phosphate (AM:JOPH), Jordan Islamic Bank (AM:JOIB), Jordan Refinery (AM:JOPT) and the Arab bank (AM:ARBK)1, the news was celebrated by economists and everyone alike, and the news was met with praise. The news became evidentially part of the “post-COVID 19 economic recovery phase” paradigm and that things were moving in the right track.

But people tend to forget that the Amman Stock Exchange itself was downgraded by MSCI on the 26th of November of 2008 from Emerging to Frontier Market2, and that since that time not a single new IPO listing took place in the stock exchange.

Will this recent re-classification be a game changer for the newly listed companies and the Jordanian financial market as a whole?

It’s all about Volume

One important parameter to being recognised internationally is daily volume, or in other words, liquidity. Since the so-called Arab Spring in 2011 and up until beginning of 2020, the daily average trading volume at the Amman Stock Exchange was around 5-6 million JODs.

Then starting in 2021, the daily average volume rose by 32% to average 8.5 million JODs.

The main driver was the Jordan Phosphate Mining Company:

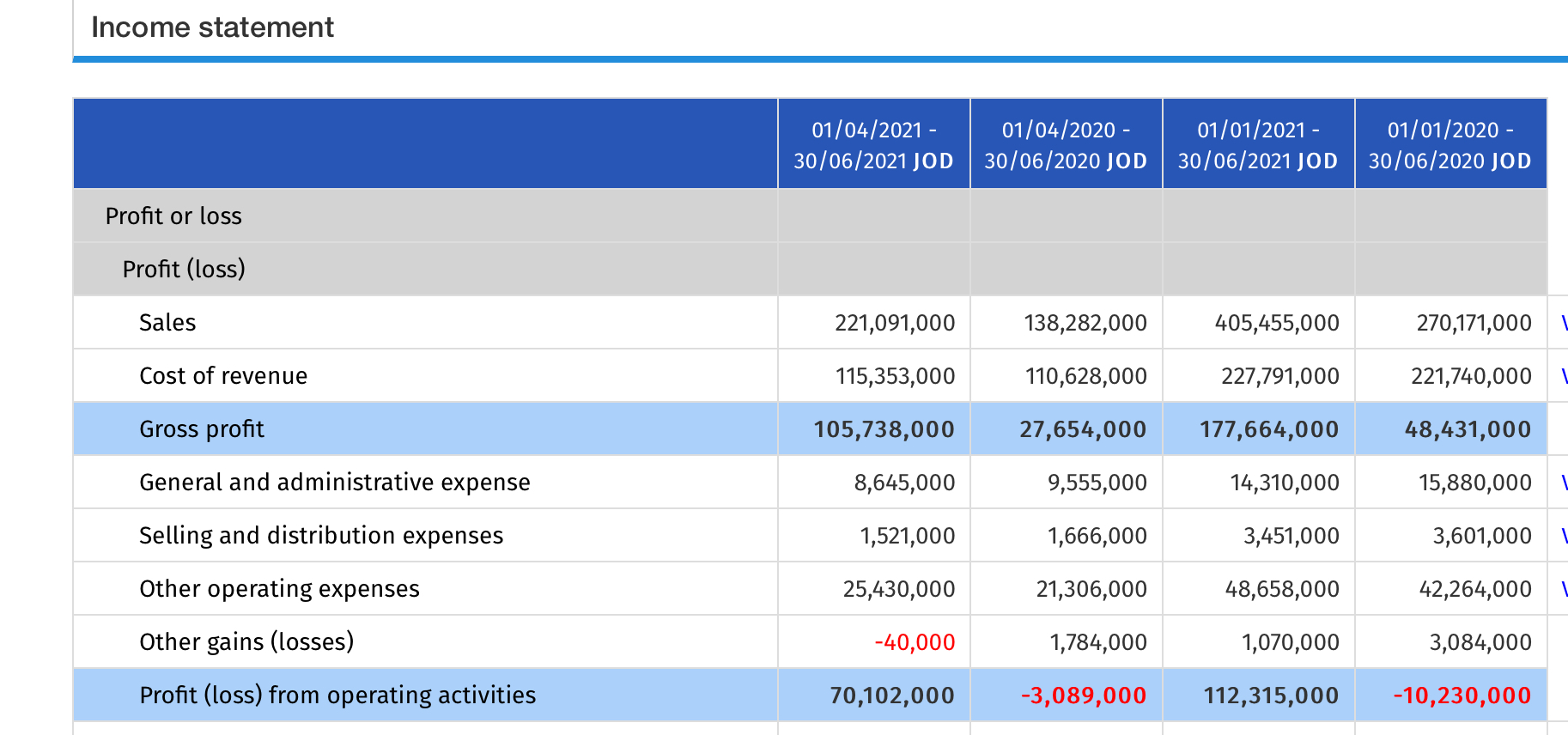

The monthly trading volume went from 1.5 million JODs in January 2020 to a peak of 58 million JODs in June of 2021. This jump can be explained by the massive surge in commodities prices all around the globe, from steel to cement to lumber as well as the end to a long marathon in court that ended in victory to the company.3

Since the pandemic, the price of Phosphate jumped more than 50% and so did the company’s revenues for H1/2021.

Actual Impact

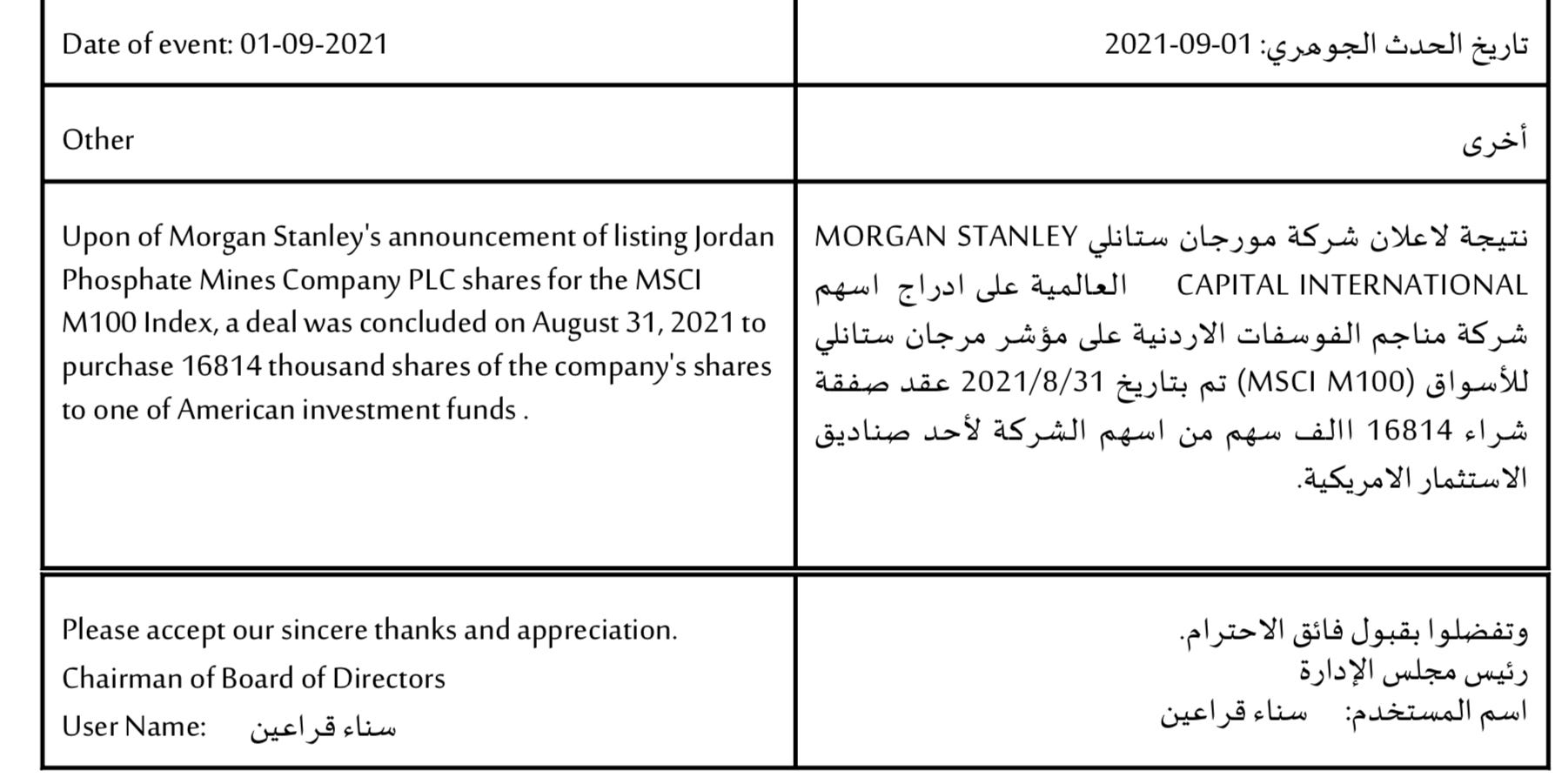

During the first month, the impact of the MSCI listing has been negligible.

New shares purchased by foreign entities were too little: only 16814 shares were sold. Still too early to tell.

The share price rose by just 1.6% in the month of September (up 6% in October).

Conclusion

COVID19 lockdowns have clearly destabilised the supply demand cycles of the commodity markets.

The energy market is evidence for this:

Prices have reached record highs for all commodities, yet a lot of economists forecast lower prices across the board once the storm has settled and markets have balanced out come spring 2022.

Even when phosphate prices are back to pre-COVID levels, the main question for the company is: will the high trading volume maintain its momentum?

If not, the company will once again be in danger of being delisted from MSCI fund.

http://www.jordantimes.com/news/local/msci-lists-4-jordanian-companies-index-emerging-markets

https://www.msci.com/our-solutions/indexes/market-classification

https://www.ase.com.jo/en/download/disclosure/100012112